Key Takeaways

- Most married couples lower their tax liability by choosing the Married Filing Jointly status, which preserves access to deductions that separate filers lose.

- When there is a significant income gap between partners, combining earnings on a joint return can pull the higher earner’s income into a lower tax bracket.

- The unique Spousal IRA rule allows a non-working spouse to legally contribute to a retirement account using their partner’s earned income.

- Dual-income married couples can cross-examine both of their workplace benefit packages to strategically choose the most lucrative mix of tax-free 401(k), HSA, and FSA perks.

- High earners and certain low-income families must plan ahead for marriage penalties triggered by shared deduction caps and compressed surtax thresholds.

When you’re planning your wedding, you’ve got a zillion things to think about: Napkin colors. Flower arrangements. Your strategy for keeping the microphone away from Dad before he gives an embarrassing speech.

Makes sense that you wouldn’t be thinking about your taxes.

But Uncle Sam has some wedding gifts for you in the form of tax perks. Here’s how saying “I do” might actually lower your overall tax bill.

Do you get better tax breaks for being married?

When you say “I do,” the IRS changes how it views your finances. Which could result in a lighter tax burden for you and your spouse-to-be. Here is a breakdown of the major tax benefits of marriage that every Chattanooga newlywed couple should know.

1. Flexible filing statuses

Once you’re married, you gain the flexibility to choose between Married Filing Jointly (MFJ) or Married Filing Separately (MFS).

For the vast majority of couples, filing a joint return is the winning strategy because you combine your income, deductions, and credits onto a single tax return, saving time and tax preparation costs.

Also, if you file separately, you can’t claim perks like the Earned Income Credit (EIC), the American Opportunity Tax Credit (for higher education), or the student loan interest deduction.

In specific scenarios, filing separately can work to your advantage. The most common trigger is high out-of-pocket medical expenses.

Medical expenses are only deductible if they exceed 7.5% of your Adjusted Gross Income (AGI). By filing separately, a spouse with high medical bills isolates their lower individual AGI, making it much easier to clear that 7.5% hurdle and claim the deduction.

However, if you choose to file separately and one spouse chooses to itemize deductions (which you must do to claim medical expenses), the other spouse is also required to itemize.

This means the second spouse forfeits their Standard Deduction, which could offset any savings gained from the medical deduction. Always run the numbers both ways.

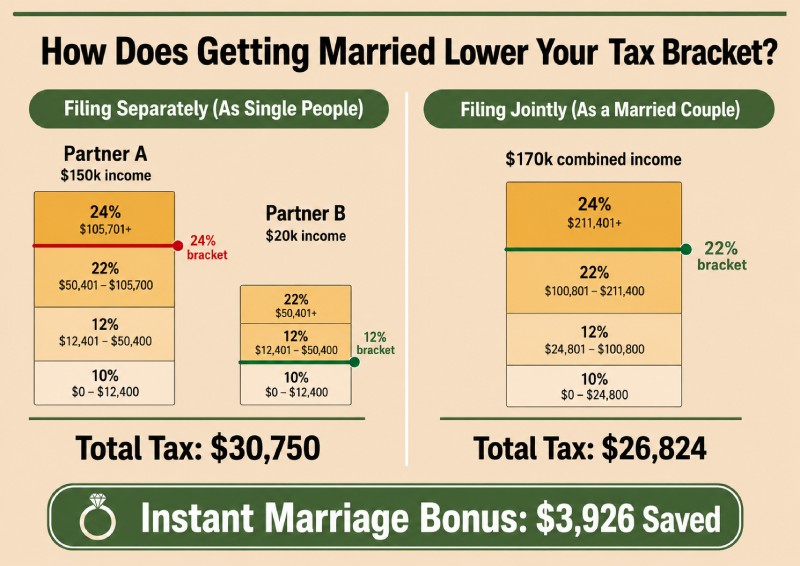

2. Lower tax brackets for unequal earners

When one spouse earns significantly more than the other, your combined income can pull the higher earner’s income down into a lower tax bracket when filing jointly.

Let’s look at how this plays out in a scenario where Taxpayer A has a taxable income of $150,000, and Taxpayer B has a taxable income of $20,000.

If they file separate individual returns, their taxes are calculated independently:

- Partner A lands in the 24% top tax bracket and owes a total of $28,598 in federal income tax.

- Partner B stays in the 12% top tax bracket and owes $2,152 in federal income tax.

- Together, their total household tax burden as single people comes out to $30,750.

But when they combine their income on a single, joint tax return:

- Their combined taxable income is now $170,000 ($150,000 + $20,000).

- A joint income of $170,000 tops out in the 22% bracket instead of the 24% bracket.

- The total federal tax owed on their combined return drops to $26,824.

3. Higher limits on charitable contribution deductions

Getting married can actually increase the amount of donations you can deduct in a single tax year.

To claim deductions for donations, you must itemize your deductions. The IRS limits your annual cash charity deductions to 60% of your Adjusted Gross Income (AGI) (and 50% for property donations). Any amount above this cap must be carried forward to future tax years.

When you file jointly, the IRS calculates your 60% limit based on your combined joint AGI, creating a much higher deduction ceiling.

4. Unlock or boost the Earned Income Tax Credit (EITC)

The Earned Income Tax Credit (EITC) is designed to reduce the tax bill for low- to moderate-income workers. To qualify for it, you can’t earn too much money, but you must have some form of earned income (like wages, salaries, or tips).

If you’re single and don’t work, you’re automatically locked out of this credit.

But because your eligibility as a married couple is based on your combined income, a non-working spouse can suddenly become eligible for the credit by marrying someone with a modest earned income.

5. Double your retirement savings with a spousal IRA

If you are single and do not work, you cannot legally contribute to a traditional or Roth Individual Retirement Account (IRA), nor can your annual contributions exceed what you earned that year.

But if you file a joint return, the “Spousal IRA” rule allows a non-working spouse to open and contribute to their own separate IRA using the working spouse’s taxable earned income.

There are a few key rules around this to be aware of:

- You must file a Married Filing Jointly return to utilize this strategy.

- The total contributions made to both your IRA and your spouse’s IRA cannot exceed the total taxable earned income reported on your joint return.

- You still cannot exceed the combined annual IRS contribution limit set for each individual spouse.

6. Access better perks

Many of the absolute best tax-saving vehicles, like 401(k) plans, Health Savings Accounts (HSAs), and Flexible Spending Accounts (FSAs), are only accessible as employee benefits provided through your Hamilton County workplace. These accounts allow you to shield your income from taxes through tax-free contributions, tax-free growth, or tax-free withdrawals.

When you’re single, you’re limited to the benefit menu your employer offers. However, when you get married and both you and your spouse are employed, you get the ability to “benefit shop.”

You can strategically review the employee benefits packages at both of your jobs and pick the absolute best mixture to maximize your household tax savings.

Are there tax disadvantages to getting married?

When couples come to me asking, “Do you get better tax breaks for being married?” I have to show them the other side of the coin: Both low-earning and high-earning couples can sometimes find themselves paying more to the IRS as a married unit than they did as two single individuals.

Here are three distinct tax disadvantages of marriage you need to watch out for.

1. The EITC marriage penalty

The EITC income limits for married joint filers are only slightly higher than those for single filers. A single taxpayer with one qualifying child can earn up to $51,593 before completely losing eligibility for the credit.

But if that same individual marries a partner who also works, their combined income limit for a joint return only moves up to $58,863 for a family with one child.

2. High earners trigger surtaxes

High-earning couples face a steep marriage penalty involving the 3.8% Net Investment Income Tax (NIIT) and the 0.9% Additional Medicare Surtax.

The IRS applies these extra surtaxes to your income once you pass a certain financial threshold. Single taxpayers are not subject to these additional taxes until their income exceeds $200,000. However, the threshold for married couples filing jointly is capped at just $250,000 total.

3. The shared SALT deduction cap

The State and Local Tax (SALT) deduction allows you to deduct property taxes, along with either state income or sales taxes, from your federal return if you itemize. The maximum amount you can deduct under the SALT cap is $40,000 per household.

The major disadvantage here is that the $40,000 cap applies equally to a single individual and a married couple filing jointly.

And filing separately doesn’t fix this, as the cap is simply split into $20,000 per spouse.

Final thoughts

Your financial picture is entirely unique from any other couple’s. And a single choice, like whether to file jointly or separately, can shift your tax liability by thousands of dollars.

And if you’re currently planning your wedding, you’ve already got too many things to think about. So let me run the numbers for you. Grab a spot on my schedule, and we’ll build a customized tax strategy for your new life together.

login.atomanager.com/atom_ust/default.aspx?redirect=webinfonewclientappointment.aspx

FAQs

“Does your wedding date affect your taxes for the entire year?”

The IRS determines your marital status based on where you stand on the very last day of the year. If you tie the knot on or before December 31, the IRS considers you married for the entire tax year, meaning you must file your upcoming return using a married status.

“Can you still file as single the year you get married?”

You cannot legally choose to file as single if you are legally married on December 31st of that tax year. Your only two legal tax options under federal law are Married Filing Jointly or Married Filing Separately.

“Is it always better to file Married Filing Jointly?”

While filing a joint return lowers the tax bill for most couples, it is not always the best choice. Filing separately can sometimes save you money if one spouse has exceptionally high out-of-pocket medical bills or if you need to keep separate incomes to lower payments on an Income-Driven Student Loan Repayment plan.

“Do you get better tax breaks for being married?”

For the vast majority of couples, getting married unlocks significantly better tax breaks and a lower overall household tax bill. Filing a joint return triggers a “marriage bonus” by widening your tax brackets, doubling your standard deduction, and allowing a non-working spouse to build retirement wealth through a Spousal IRA. It also creates a higher joint income ceiling, making it much easier to fully deduct large charitable contributions in a single year.

“Do I need to update my W-4 tax form immediately after getting married?”

You should submit a revised Form W-4 to your employer’s payroll department shortly after getting married. Combining your incomes can drastically change your household tax bracket, and adjusting your federal income tax withholding early prevents you from facing a surprise tax bill or penalty at the end of the year.

“How do we change our names with the IRS after marriage?”

You do not actually notify the IRS directly about a name change; instead, you must update your name with the Social Security Administration (SSA). Once the SSA processes your marriage certificate and legal name change, they will automatically update the IRS database, ensuring your tax return isn’t rejected due to a name mismatch.